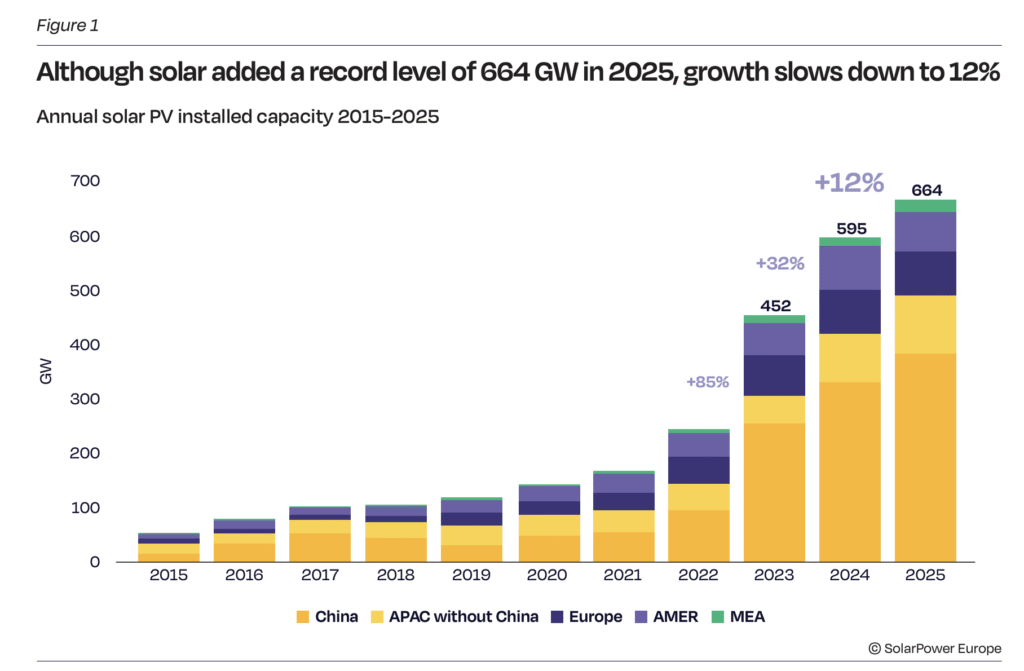

The global solar market added a record 664 GW of solar in 2025, according to SolarPower Europe’s Global Solar Market Outlook 2026-2030.

The figure repesents an increase of 69 GW compared with 2024 and 212 GW compared to 2023 but indicates that annual market growth is slowing, from 85% in 2023 and 32% in 2024 to 12% last year.

The Asia-Pacific accounted for 487 GW, or 73%, of solar added last year, with China alone installing 382 GW for a record 57% market share. India added 45.7 GW, overtaking the United States as the second largest solar market.

Europe installed 81.6 GW of solar last year, a 3% year-on-year increase, led by Germany as the fourth largest global market. The Americas added 43.2 GW, a 13% year-on-year decline, while the Middle East and Africa added 23.7 GW, a 51% increase on installations in 2024.

The ten largest markets last year – China, India, US, Germany, Brazil, Spain, Saudi Arabia, France, Italy and Japan – accounted for 82% of new solar installations in 2025.

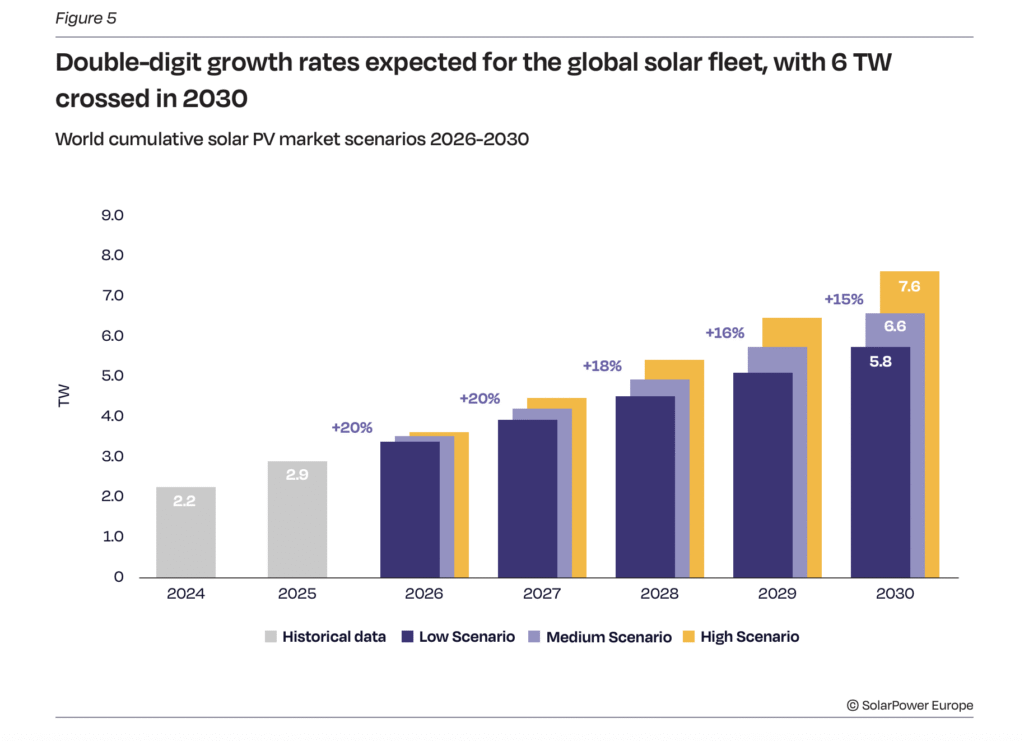

Growth has continued into this year, with SolarPower Europe reporting that total global capacity passed the 3 TW milestone earlier this year, less than two years after reaching 2 TW and four years after surpassing 1 TW. Solar now supplies 9% of global electricity demand, three times as much as five years ago.

Despite this momentum, the report is forecasting annual global solar installations to decline this year. An estimated 612 GW is expected under a medium scenario, which would represent an 8% annual decrease and mark the first contraction in over 20 years.

SolarPower Europe explains this downturn is largely driven by China, which is on course to record a 24% reduction in installations following policy changes. “The decline outweighs continued growth in all other regions, highlighting China’s influence on global installations,” the report says, before adding that the global decline should not be mistaken for a structural slowdown.

Installations in the Asia-Pacific outside of China are expected to increase by 18% this year, while Europe’s solar deployment is forecast to grow by around 3%. Solar deployment in the Americas is set to expand by 11% this year, the report adds, while installations are expected to surge 48% in the Middle East and Africa.

The report’s medium scenario forecasts global solar capacity to more than double to 6.6 TW by the end of the decade, a downward revision from last year’s forecast of 7.1 TW. It cites grid congestion, insufficient storage, limited system flexibility, permitting delays, financing barriers and supply-chain resilience as key challenges hampering further growth.

“While short-term uncertainties persist, the long-term outlook for solar remains strong, with the technology continuing to expand at an unprecedented pace and cementing its role at the core of global decarbonisation efforts, and its new role as the key technology for countries striving for more energy security,” the report adds.

It also highlights solar’s role amid geopolitical tensions and a second fossil fuel crisis in less than four years. In 2025, the electricity generated by solar was equivalent to nearly five years of liquefied natural gas flows through the Strait of Hormuz.

Solar accounted for around 80% of reneweable capacity additions last year while outpacing the combined additions of fossil fuel and nuclear power generation. “These remarkable achievements reflect the extraordinary pace at which solar has become the backbone of the global energy transition,” the report says.

Walburga Hemetsberger, CEO of SolarPower Europe, commented that the slowdown in growth observed in 2025 and the expected drop in 2026 are important signals highlighting a new reality.

“Scaling solar is no longer just about deploying more capacity but about how well it can be integrated into the system,” Hemetsberger said.

“We urgently need to invest in grids, battery storage, and other non-fossil flexibility solutions to continue integrating large volumes of renewables into our grids,” Hemetsberger added. “If policymakers address these challenges, solar will continue to lead the energy transition and remain the most powerful tool to deliver energy security, competitiveness, and decarbonisation.”

Source link